Table Of Content

- Home Equity Loan Vs. Personal Loan: What’s The Best Option?

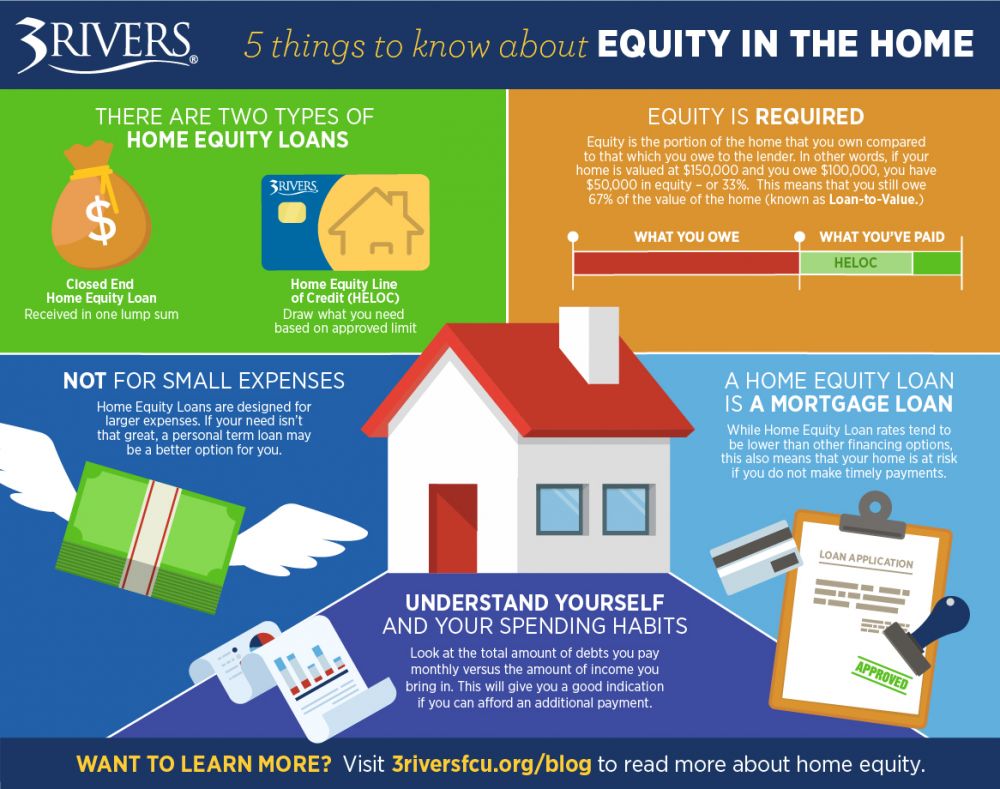

- How To Get A Home Equity Loan

- Cons to Using A Home Equity Loan to Buy A Second Home

- DOJ Office for Victims of Crime Funding to Print Child Victims and Witnesses Support Materials Now Open

- National Strategy for Suicide Prevention

- Home improvements can add value to your home and increase equity

While you may benefit from a lower rate by using your equity to consolidate debt, remember that you’re risking your home. If you don’t repay the equity you borrowed as you agreed, your lender could foreclose on your home to get paid. As we noted, by using your home equity to consolidate your debt, you’ll pay a lower interest rate than with unsecured loans. When you use your home equity to get a loan, the lender has rights to your home if you don’t pay as agreed. However, before you make extra mortgage payments, ensure your lender doesn’t impose prepayment penalties for paying off the principal earlier than planned.

Home Equity Loan Vs. Personal Loan: What’s The Best Option?

Her expertise is in personal finance and investing, and real estate. Once you have the appraised value of your home and the outstanding balance of your mortgage, calculate your home equity by subtracting the mortgage balance from the home value. You can find this information on your most recent mortgage statement.

How To Get A Home Equity Loan

It follows that if your property increases in value, so too will the amount of equity you hold. Similarly, if you have a repayment mortgage, the idea is that, over time, the level of equity you own in your property will increase as you pay off your mortgage. This means that as baseline interest rates go up or down, the interest rate on your HELOC will adjust, too. However, because a HELOC is secured against the value of your home, the interest is typically lower than the rate you’d pay on a credit card or personal loan, and closer to a mortgage rate. Also, when deciding if you should use your home equity to consolidate debt, consider how long you need to repay the debt. Even though the rate is lower on a loan secured by your home, you may pay more interest over time if you have a longer repayment term (e.g., 15 years versus three years).

Cons to Using A Home Equity Loan to Buy A Second Home

Your home is also likely to be one of the most valuable assets you will own. Unlike some investments, home equity cannot be quickly converted into cash. That's because the equity calculation is based on a current market value appraisal of your property. That appraisal is no guarantee that the property would sell at that price.

Rocket Mortgage® is now offering home equity loans, which are available for primary and secondary homes. As you pay down your balance, a higher proportion of your monthly payment goes toward the principal balance instead of interest. This process, called amortization, helps you build equity faster toward the end of your loan term. Your equity reveals the percentage of your home’s value that you can rightfully claim as your own. If you’re a homeowner, simply making your mortgage payments on time each month is a quick way to build your equity. Unlike primary mortgages that tend to be paid off over a 30-year period, home equity loans and HELOCs are often used for a shorter amount of time.

10 Reasons To Use Home Equity - Bankrate.com

10 Reasons To Use Home Equity.

Posted: Mon, 25 Mar 2024 07:00:00 GMT [source]

To determine whether you qualify and how much money you can borrow, a lender will have your home appraised. The home appraisal will tell the lender how much your home is worth. You can calculate your home equity by subtracting your mortgage’s principal balance from the estimated market value of your home. If you believe you’ve reached 20% equity because your home’s value increased, you can contact your lender to remove PMI as well.

National Strategy for Suicide Prevention

Afterward, you pay this fixed-rate loan back in regular monthly installments with interest while continuing to make your monthly payments on your original mortgage. On the other hand, a home equity loan is a lump sum loan with a fixed interest rate and fixed monthly payments. You borrow a set amount of money and pay it back over the life of the loan. Since home equity loans come with fixed interest rates, your monthly payments will never change, and you’ll know exactly how much you need to budget to repay the loan.

Requirements for a Home Equity Loan or HELOC in 2024 - CNET

Requirements for a Home Equity Loan or HELOC in 2024.

Posted: Fri, 12 Apr 2024 07:00:00 GMT [source]

This margin varies among lenders, so it’s in your best interest to shop around for quotes. No matter which lender you choose, borrowers with higher credit scores and lower debt-to-income ratios are more likely to qualify for the best rates. You’ll receive the full amount at closing, and you’ll repay the home equity loan — principal and interest each month — at a fixed rate over a set number of years. Be sure that you can afford this second mortgage payment in addition to your current mortgage, as well as your other monthly expenses.

Alternative Financing Options To Buy Another House

Estimate your home’s current value by comparing it with recent sales in your area or using an estimate from a site like Zillow or Redfin. Be aware that their value estimates are not always accurate, so adjust your estimate as needed considering the current condition of your home. Then divide the current balance of all loans on your property by your current property value estimate to get your current equity percentage in your home. Should you want to relocate, you might end up losing money on the sale of the home or be unable to move.

If you’ve built up equity in your home and have a strong credit score and a low debt-to-income ratio, a home equity loan may be beneficial for you. It will enable you to take out a large lump sum that you can pay off over an extended period. Unlike home equity loans, HELOCs have variable interest rates, which are similar to adjustable-rate loans.

In the early years of homeownership, the largest portion of your payment is applied to interest, resulting in you building equity at a slower pace. But as the life of the loan progresses, you see more of your payment applied to your principal, which pays down your balance faster. This flip occurs because the interest you are charged each month is calculated using your outstanding balance, which gets smaller with every payment you make. With a cash-out refinance, you’ll take out a mortgage for a higher amount than what you owe on your home.

The Federal Trade Commission’s final rule banning noncompete provisions in contracts will have broad implications for employers and employees in the labor and employment context. It will also impact businesses and their owners entering into sale transactions and any other transactions involving noncompetes. If you’re an older homeowner who wants to unlock the equity in your home, equity release or remortgaging could both be explored.

No comments:

Post a Comment